'%3E%3Cpath%20fill='%231B2A47'%20d='M1.605%2016.263c.03-1.139.059-2.482.088-3.971.03-1.49.03-2.832.03-4.03%200-.758%200-1.576-.03-2.51%200-.905-.03-1.84-.03-2.803%200-.496-.028-.964-.028-1.43%200-.468%200-.906-.03-1.315h6.858q2.188%200%203.589.35c.963.234%201.663.643%202.13%201.198.496.555.73%201.372.73%202.394%200%20.788-.176%201.46-.497%201.985-.32.526-.846.935-1.575%201.197-.73.292-1.693.468-2.918.526v.263c1.313.087%202.334.263%203.122.525.758.263%201.342.672%201.692%201.197.35.526.525%201.197.525%202.044%200%201.08-.233%201.927-.67%202.57-.468.642-1.139%201.08-2.102%201.343-.933.262-2.159.408-3.705.408H1.605zm6.537-9.197q1.882%200%202.713-.526c.555-.35.817-.934.817-1.752%200-.905-.292-1.547-.846-1.927s-1.459-.554-2.655-.554H4.757v4.759zm.204%206.92c.934%200%201.663-.088%202.217-.263.555-.176.934-.438%201.197-.818s.38-.876.38-1.518c0-.876-.322-1.49-.934-1.84-.643-.35-1.635-.525-3.035-.525H4.757v4.963zM21.038%2016.555c-1.576%200-2.801-.292-3.618-.905-.817-.614-1.284-1.519-1.372-2.745-.087-1.226.205-2.774.847-4.613s1.43-3.358%202.392-4.584c.963-1.226%202.043-2.131%203.298-2.744C23.839.292%2025.24%200%2026.786%200c1.576%200%202.772.321%203.59.934.816.613%201.283%201.548%201.37%202.774s-.203%202.774-.845%204.613c-.642%201.81-1.43%203.358-2.393%204.584s-2.072%202.132-3.297%202.745a9.8%209.8%200%200%201-4.173.905m.788-2.278c.642%200%201.138-.058%201.371-.116.205-.059.496-.117.847-.322.262-.146.437-.292.554-.408.204-.175.32-.292.438-.41.204-.203.35-.408.496-.583.35-.438.642-.876.963-1.402.233-.408.466-.817.67-1.284.205-.438.38-.905.555-1.372.438-1.198.671-2.278.671-3.183s-.204-1.606-.612-2.131c-.409-.497-1.051-.76-1.897-.76-.467%200-.934.059-1.43.205h-.03c-1.02.292-1.925%201.226-2.042%201.372-.116.117-.467.526-.963%201.343a15.5%2015.5%200%200%200-1.342%202.92c-.408%201.197-.642%202.277-.671%203.182-.03.906.175%201.636.584%202.161q.611.788%201.838.788M14.853%2038.54c-1.576%200-2.802-.292-3.619-.905s-1.284-1.518-1.371-2.744c-.088-1.227.204-2.774.846-4.614s1.43-3.357%202.393-4.584%202.042-2.13%203.297-2.744c1.255-.613%202.655-.905%204.173-.905%201.575%200%202.772.321%203.589.934s1.284%201.548%201.371%202.774c.088%201.226-.204%202.774-.846%204.613-.642%201.81-1.43%203.358-2.393%204.584s-2.072%202.131-3.297%202.745c-1.226.613-2.626.846-4.143.846m.787-2.277c.642%200%201.138-.059%201.372-.117.204-.058.496-.117.846-.321.263-.146.438-.292.554-.409.205-.175.321-.292.438-.409.204-.204.35-.408.496-.584a13%2013%200%200%200%201.634-2.686c.204-.438.38-.905.555-1.372.437-1.197.67-2.277.67-3.182%200-.906-.203-1.606-.612-2.132-.409-.496-1.05-.759-1.897-.759-.467%200-.934.058-1.43.204h-.029c-1.021.292-1.925%201.227-2.042%201.373-.117.116-.467.525-.963%201.343a15.5%2015.5%200%200%200-1.342%202.92c-.409%201.196-.642%202.277-.671%203.182s.175%201.635.583%202.16q.613.789%201.838.789'/%3E%3Cpath%20fill='%23FF515E'%20d='M55.966%2038.57c-1.576%200-2.801-.293-3.618-.906s-1.284-1.518-1.372-2.744c-.087-1.227.204-2.774.846-4.613s1.43-3.358%202.393-4.584c.963-1.227%202.043-2.132%203.297-2.745s2.656-.905%204.173-.905c1.576%200%202.772.321%203.589.934s1.284%201.548%201.371%202.774c.088%201.226-.204%202.774-.846%204.613-.642%201.81-1.43%203.358-2.393%204.584s-2.071%202.131-3.297%202.745c-1.225.613-2.626.846-4.143.846m.788-2.249c.642%200%201.138-.058%201.371-.117.204-.058.496-.116.846-.32.263-.147.438-.293.555-.41a7%207%200%200%200%20.437-.408c.205-.205.35-.41.496-.584a13%2013%200%200%200%201.634-2.686c.205-.438.38-.905.555-1.373.438-1.197.671-2.277.671-3.182s-.204-1.606-.613-2.131c-.408-.497-1.05-.76-1.896-.76-.467%200-.934.059-1.43.205h-.03c-1.02.292-1.925%201.226-2.042%201.372-.117.117-.467.526-.963%201.343a15.5%2015.5%200%200%200-1.342%202.92c-.409%201.197-.642%202.277-.671%203.182s.175%201.635.583%202.16q.614.79%201.839.79'/%3E%3Cpath%20fill='%231B2A47'%20d='M33.06%2016.263c0-.35%200-.935.03-1.81.029-1.051.058-2.103.058-3.154s.03-2.073.03-3.007c0-1.606-.03-3.27-.06-4.993%200-.554-.028-1.08-.028-1.606%200-.525-.03-1.021-.03-1.46h6.828c1.46%200%202.685.117%203.59.38q1.4.394%202.1%201.314.7.963.7%202.628c0%20.992-.174%201.81-.554%202.452-.35.643-.904%201.11-1.604%201.431s-1.576.467-2.627.496v.263q2.058.087%203.064.876c.671.525%201.138%201.372%201.43%202.51.087.41.233%201.023.467%201.84.233.818.408%201.431.554%201.84h-3.414a11%2011%200%200%200-.262-1.022c-.321-1.314-.526-2.19-.584-2.628a5%205%200%200%200-.642-1.46%202.13%202.13%200%200%200-.963-.73c-.408-.146-.934-.233-1.605-.233h-3.326v6.0440000000000005H33.06zm6.332-8.292c1.343%200%202.276-.205%202.86-.613.554-.41.846-1.11.846-2.073%200-.73-.146-1.314-.408-1.723-.263-.409-.671-.7-1.197-.876q-.788-.263-2.1-.263h-3.181v5.519h3.18zM49.4%2016.263l.03-2.745c.029-2.452.029-4.905.029-7.416q0-2.101-.088-5.868h4.085l5.924%2010.335c.087.234.204.438.291.643.117.204.205.408.321.613.38.788.613%201.255.672%201.372h.262c0-.058-.03-.146-.03-.204%200-.059-.028-.117-.028-.175a75%2075%200%200%201-.175-1.314%2010%2010%200%200%201-.088-1.285c0-1.547%200-3.737-.029-6.57V1.84c0-.584-.03-1.11-.03-1.576h2.977c-.03%202.482-.058%205.08-.058%207.766%200%201.694%200%204.438.029%208.292h-4.027l-5.573-9.43c-.875-1.81-1.226-2.511-1.05-2.132-.263-.613-.467-1.08-.613-1.46h-.263c.058.35.117.876.175%201.548.059.7.117%201.168.117%201.46%200%202.978%200%206.306.029%209.985H49.4zM4.698%2038.277c.029-2.627.058-5.255.058-7.883%200-1.576%200-3.503-.029-5.752-1.109%200-2.684%200-4.727.03v-2.453h12.664v2.453c-1.955-.03-3.53-.03-4.756-.03%200%20.584-.03%201.227-.03%201.957s0%201.46-.029%202.218v1.84c0%202.57.03%205.11.059%207.62z'/%3E%3Cpath%20fill='%23FF515E'%20d='M29.441%2038.277c.409-1.05.788-2.102%201.168-3.182s.787-2.16%201.167-3.241c.613-1.693%201.05-2.949%201.342-3.766l1.255-3.65c.116-.38.262-.788.379-1.139.117-.38.263-.73.38-1.05h4.61l-.671%2012.904h.262l8.316-12.905h4.669l-.7%201.869c-.876%202.452-1.343%203.766-1.43%204a501%20501%200%200%200-3.385%2010.16h-2.947c.292-.846.788-2.219%201.459-4.087.175-.526.35-1.08.554-1.606.175-.526.38-1.08.555-1.577.642-1.81%201.342-3.825%202.072-6.014h-.234l-8.724%2013.314h-2.86l.554-13.314h-.175c-.175.496-.38.992-.554%201.489-.175.496-.38%201.022-.555%201.547a163%20163%200%200%200-1.08%203.008c-.145.38-.262.759-.408%201.138-.117.38-.262.73-.408%201.11-.7%201.898-1.284%203.59-1.751%205.05h-2.86zM68.047%2038.277c.175-2.19.32-4.525.467-7.007.058-.905.204-3.912.467-9.051h3.151c-.03.438-.058.934-.088%201.46s-.058%201.08-.087%201.693a264%20264%200%200%201-.409%206.657c-.145%201.986-.35%203.591-.583%204.788h.175Q72.147%2034.892%2073.94%2032a562%20562%200%200%201%204.465-7.066c.32-.496.641-.992.933-1.46s.555-.875.817-1.255h3.268q-.568.832-1.138%201.752c-.408.613-.787%201.255-1.196%201.927-3.88%206.014-6.478%2010.131-7.85%2012.35h-5.193zM79.106%2038.277c.32-.788.758-2.014%201.37-3.65a287%20287%200%200%200%201.577-4.32c.437-1.256.904-2.628%201.4-4.088s.934-2.774%201.313-3.97h11.322l-.846%202.364H87.1l-1.664%204.847%207.645-.088-.612%201.694-7.587-.088-1.75%204.934h8.286l-.846%202.365z'/%3E%3C/g%3E%3Cdefs%3E%3CclipPath%20id='a'%3E%3Cpath%20fill='%23fff'%20d='M0%200h96v40H0z'/%3E%3C/clipPath%3E%3C/defs%3E%3C/svg%3E)

A collision involving a rental vehicle like U-Haul is not the same as a typical road incident. The size, weight, and insurance structure change how responsibility is determined and how claims are handled. If you are unsure what to do after a truck accident, the right actions taken in the first minutes will directly affect liability, insurance payouts, and potential legal consequences.

This guide explains practical steps, real risks, and how U-Haul accident coverage actually works—based on real-world scenarios rather than generic advice.

What Happens When a Truck Hits a Car?

When comparing a rental vehicle and a passenger car, the difference is immediate. Larger vehicles are heavier, taller, and built with stronger materials. As a result, what happens when a truck hits a car often looks unbalanced: the smaller vehicle absorbs most of the visible damage.

Even at low speeds, impact can crush bumpers, mirrors, or panels. The rental vehicle itself may show minimal external damage, which sometimes leads drivers to underestimate the seriousness of the situation.

Why Trucks Usually Take Less Damage

Rental vehicles are reinforced, especially box models. Unlike cars, which are designed with crumple zones, these vehicles distribute impact differently. The height difference also means contact points are often above the most reinforced parts of a car.

This explains why what happens when a truck hits a car is often more severe for the smaller vehicle—even in minor collisions. According to the National Highway Traffic Safety Administration (NHTSA), 71 percent of people killed in crashes involving large trucks were occupants of the other vehicles—not the truck itself.

“Of the people killed in crashes involving large trucks, 71 percent were occupants of other vehicles involved in the crash.”

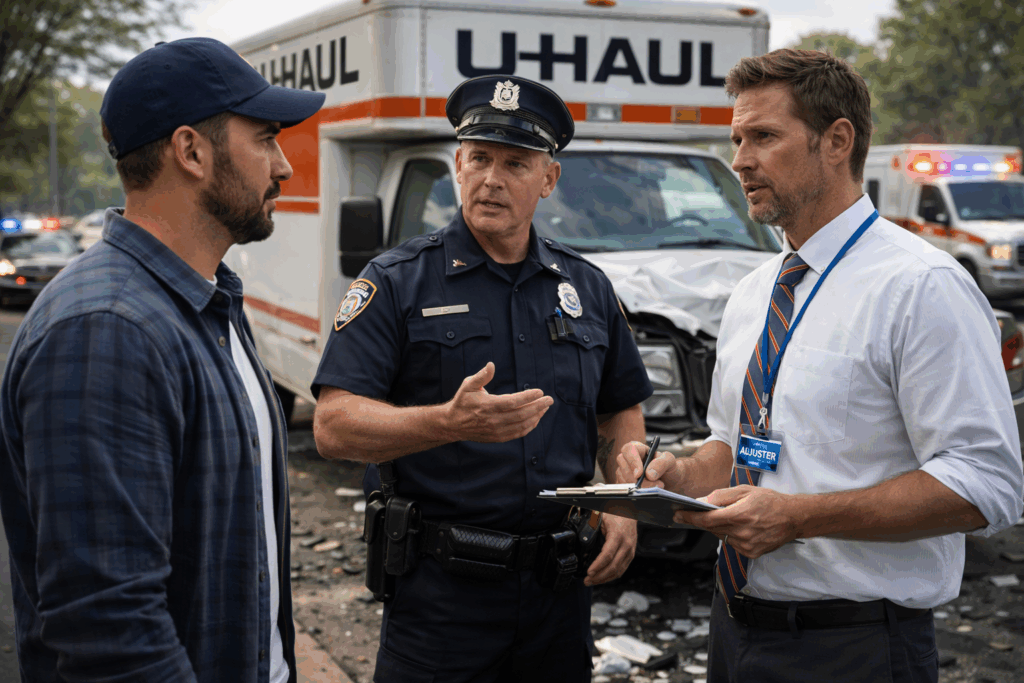

What to Do After a Truck Accident

Knowing what to do in a truck accident is not just about safety—it protects you legally and financially. Missing even one step can complicate insurance claims or lead to penalties.

Step-by-Step Action Guide

| Step | What to Do | Why It Matters |

|---|---|---|

| 1 | Call the police | Creates an official accident report |

| 2 | Take photos of all damage | Provides evidence for insurance claims |

| 3 | Exchange information | Required for legal and insurance purposes |

| 4 | Do not leave the scene | Avoids hit-and-run charges |

| 5 | Contact your insurance provider | Starts the claims process |

These steps define what to do after a truck accident in a way that insurance companies and law enforcement expect.

Truck Driver Accident Procedures You Must Follow

Even if you are not a professional driver, once you operate a rental vehicle, expectations are similar. Basic truck driver accident procedures include:

- Call the police immediately

- Take clear photos of both vehicles and surroundings

- Exchange driver’s license and insurance details

Skipping any of these can delay or weaken your claim.

What to Do If You Hit a Parked Car

This is a common situation with rental vehicles due to blind spots and turning radius. If you hit a parked car and no one is present:

- Take photos of the damage

- Leave your phone number clearly visible

- Do not leave without identification

Driving away may be treated as a hit-and-run, even if the damage seems minor.

Who Is Liable in a U-Haul Accident?

Responsibility depends on how the incident happened. In many cases—such as at traffic lights or intersections—the police and insurance companies determine fault.

However, if you are driving a rental vehicle, you are typically responsible unless proven otherwise. This is especially important if you did not purchase U-Haul accident insurance.

Insurance companies assess multiple factors:

- Traffic violations

- Driver behavior

- Vehicle positioning

- Witness reports

U-Haul Accident Insurance: What You Need to Know

Understanding U-Haul accident coverage is critical before and after an incident. Many renters assume they are fully protected, which is not always accurate.

U-Haul Insurance Coverage Comparison

| Coverage Type | What It Covers | Typical Limit | Notes |

|---|---|---|---|

| Liability Coverage | Damage to other vehicles/property | Up to $50,000+ | Required in most cases |

| Collision Coverage | Damage to the U-Haul vehicle | Varies | May include deductible |

| Full Protection | Both U-Haul and third-party damage | Higher limits | Most comprehensive option |

| Overhead Damage Coverage | Roof and bridge impact | Limited | Often not included by default |

What Happens If You Don’t Have Insurance

If you decline coverage, you are fully responsible. This includes:

- Damage to the rental vehicle

- Damage to other vehicles

- Property damage

In some cases, your personal auto insurance may apply—but only if your policy includes rental vehicle coverage.

Does Your Personal Insurance Cover a U-Haul Accident?

Some personal policies extend to rental vehicles, but not all. Before relying on it, you must confirm:

- Coverage limits

- Vehicle size restrictions

- Deductibles

Assuming coverage without verification is a common and costly mistake.

Coverage Limits and Deductibles

Even when covered, policies have limits. For example:

- Liability may cap at $50,000

- Deductibles can apply to collision claims

- Excess damage must be paid out of pocket

This becomes critical in serious cases where repair costs exceed limits.

Financial Responsibility in a Rental Truck Accident

Who pays depends on your coverage and the extent of damage.

Who Pays for Damage

| Scenario | Who Pays |

|---|---|

| You purchased U-Haul coverage | U-Haul insurance (within policy limits) |

| Your personal auto insurance applies | Your insurance provider |

| No insurance coverage | You pay out of pocket |

| Damage exceeds coverage limits | You pay remaining balance |

This is where many U-Haul accident settlement situations become complicated—especially when multiple parties are involved. Before deciding to rent a truck, it’s worth reviewing the actual moving prices of a professional service—in many cases the cost difference is smaller than expected, while the liability exposure with a rental is significantly higher.

What Happens If No One Is Around After the Accident?

If you hit a vehicle and no one is present, you still have legal obligations. Document everything carefully and leave your contact details.

Ignoring the situation increases liability and may escalate the case significantly.

Is It Considered a Hit and Run?

Yes, if you leave without attempting to identify yourself. Even minor damage can lead to serious legal consequences if reported by witnesses or cameras.

U-Haul Driving Risks: What Causes Truck Accidents?

Driving a rental vehicle is very different from driving a standard car. Many first-time renters underestimate the size and behavior of the vehicle.

Common risks include:

- Blind spots

- Wide turning radius

- Misjudging vehicle size

This is precisely why businesses opt for commercial moving services rather than renting trucks themselves—professional drivers are trained for large vehicle operation and carry full insurance coverage, eliminating this category of risk entirely.

The scale of the problem is significant. The Federal Motor Carrier Safety Administration (FMCSA) reports an average of 4,000 fatalities and over 400,000 police-reported crashes involving heavy vehicles each year in the United States.

“With an average of 4,000 fatalities and over 400,000 police-reported crashes involving heavy vehicles occurring each year, NHTSA is aggressively pursuing research related to heavy vehicle safety.”

Common Causes of Truck Accidents

| Cause | Description | Risk Level |

|---|---|---|

| Blind spots | Large invisible zones | High |

| Wide turns | Cutting corners | High |

| Misjudging size | Vehicle wider/longer than expected | High |

| Low clearance | Bridges, parking structures | Very high |

| Inexperience | First-time drivers | High |

Understanding what causes truck accidents helps prevent them. It also explains what causes most semi truck accidents, especially among inexperienced drivers.

Overhead Damage: What Happens If a U-Haul Hits a Bridge?

One of the most expensive mistakes is hitting a low bridge or structure. Rental vehicles are often around 11 feet tall, and misjudging clearance leads to severe damage.

Overhead Damage Cost Breakdown

| Damage Type | Estimated Cost |

|---|---|

| Minor roof damage | $1,000–$5,000 |

| Major structural damage | $10,000+ |

| Full box replacement | $10,000–$20,000+ |

| Bridge/property damage | Varies (can be very high) |

Low Clearance Accidents and Costs

These situations are not rare and often result in full replacement of the cargo box. Repairs are rarely partial—replacement is standard due to structural integrity requirements.

Does U-Haul Cover Overhead Damage?

Standard policies often exclude overhead damage unless specific protection is purchased. Without it, you are fully responsible.

This is one of the most overlooked gaps in U-Haul accident coverage.

Can U-Haul Refuse to Rent to You After an Accident?

Yes, under certain conditions. Whether U-Haul can refuse to let you rent a truck after an accident depends on:

- Severity of the incident

- History of previous issues

- Outstanding claims or unpaid damages

Repeated problems or serious negligence can lead to rental restrictions.

FAQ About U-Haul and Truck Accidents

How long does it take to settle a semi truck accident?

How often do trucking accidents happen?

How long does a chargeable accident stay on your record as a truck driver?

If a truck driver is in an accident does he lose his CDL?

If a truck has a small accident will it appear on the title?

Does renters insurance cover damage in a U-Haul accident?

Final Notes

Handling a rental vehicle incident correctly is not complicated—but it requires attention and discipline. The combination of size, liability, and insurance structure makes these situations more serious than standard car collisions.

If you understand what to do after a truck accident, follow proper procedures, and choose the right U-Haul accident coverage, you significantly reduce financial and legal risks.

The safest way to avoid these risks altogether is to work with a professional moving company. Born to Move handles local moves across Boston, interstate relocations across state lines, and commercial moves for businesses of any size—with trained crews, proper equipment, and full insurance on every job.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}